Tutorial 1.c.1 Conformal (Interval) Prediction: From any Prediction to Valid Intervals¶

1. Offline Conformal Prediction¶

One of the basic requirement for an interval prediction is coverage. For example, an interval prediction has 95% coverage if the true label belongs to the predicted interval for 95% of the samples. In this tutorial we will show how to generate interval predictions with provably correct coverage. In particular, we assume we also have some type of prediction (it could be any type of predictions such as point/ensemble), and we would like to transform such predictions into interval predictions.

The technique we use is called conformal prediction. We will focus on how to use conformal prediction (rather than how it works, which are introduced in many tutorials such as SV or AB). We will think of conformal prediction as a (black box) algorithm that take as input a batch of original predictions (that can be any type including ensembles) and outputs a batch of interval predictions. Of course, there is no magic without data — conformal prediction algorithm needs to a batch of labeled validation data (i.e. a batch of original prediction / label pair). However, conformal prediction is extremely data efficient, and typically only require less than 50 samples (unless we want extremely high coverage).

The main workhorse for conformal prediction is the class

torchuq.transform.conformal.ConformalIntervalPredictor. We first

import it the class, as well as some test prediction data (same as

tutorial 1.a).

# As before we first setup the environment and load the test prediction

import sys

sys.path.append('../..') # Include the directory that contains the torchuq package

import torch

from matplotlib import pyplot as plt

reader = torch.load('pretrained/boston_pretrained.tar') # Load the pretrained predictions

# Split the data into validation and test, in this example we will use quantile predictions as the original predictions

val_preds = reader['predictions_quantile'][:50]

val_labels = reader['labels'][:50] # Load the true label (i.e. the ground truth housing prices)

test_preds = reader['predictions_quantile'][50:]

test_labels = reader['labels'][50:] # Used for testing

from torchuq.transform.conformal import ConformalIntervalPredictor

To use ConformalIntervalPredictor there are only three functions

that you need to know

Constructor:

calibrator = ConformalIntervalPredictor(input_type='quantile'), there is only one required argument, which is the prediction type, it is one of the types introduced in tutorial 1.a.Train:

ConformalIntervalPredictor.train(val_preds, val_labels)trains the conformal predictor based on validation predictions and validation labelsTest:

test_intervals = ConformalIntervalPredictor.__call__(test_preds)outputs the valid interval predictions

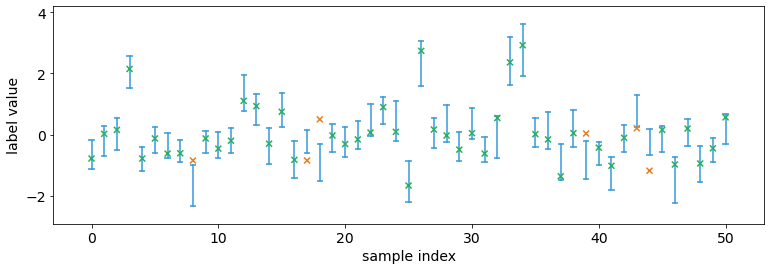

calibrator = ConformalIntervalPredictor(input_type='quantile', coverage='exact')

calibrator.train(val_preds, val_labels)

test_intervals = calibrator(test_preds, confidence=0.9)

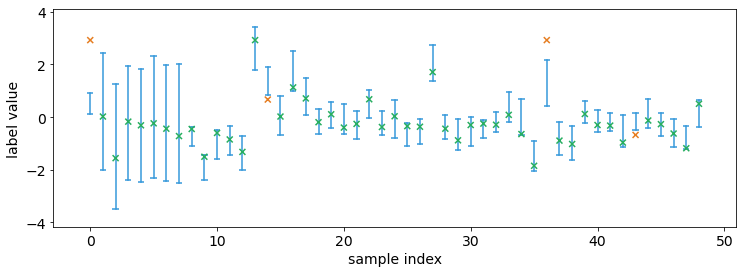

We can visualize the intervals. Observe that approximately 90% of the

labels are within the predicted confidence interval, which is equal to

our confidence=0.9. This is not a conincidence, as conformal

prediction can guarantees coverage if the data is i.i.d. (in fact, it

only requires exchangeability).

from torchuq.evaluate import interval

interval.plot_interval_sequence(test_intervals, test_labels)

There is an argument called coverage when creating the

ConformalIntervalPredictor class. If you choose coverage=exact then

the intervals have perfectly correct coverage in expectation (the

probability that the label belongs to a predicted interval is exactly

equal to confidence). If you choose coverage=1/N then the

coverage is  where

where  is the number of

validation samples.

is the number of

validation samples.

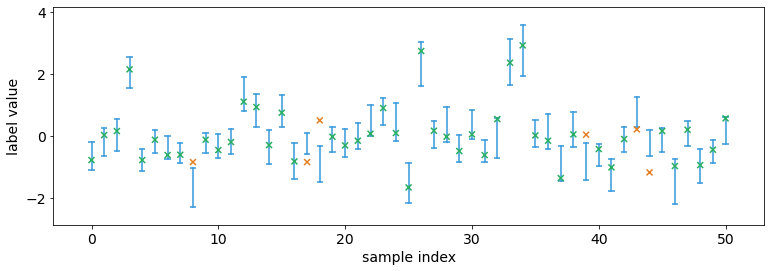

What’s the trade-off? Typically you get smaller intervals if

coverage=1/N compared to coverage=exact. For example, the

following code uses coverage=1/N and the intervals are smaller. In

fact, if you use coverage=exact and have less than 1/confidence

validation samples, the calibrator might predict an infinitely large

interval and output ![[-\infty, +\infty]](../../_images/math/b9eeeb613a8b1b7c3928d2e606cf58313fc8fb32.png) . On the other hand, if

you choose

. On the other hand, if

you choose coverage=1/N then the calibrator will never predict an

infinitely large interval.

calibrator = ConformalIntervalPredictor(input_type='quantile', coverage='1/N')

calibrator.train(val_preds, val_labels)

test_intervals = calibrator(test_preds, confidence=0.9)

interval.plot_interval_sequence(test_intervals, test_labels)

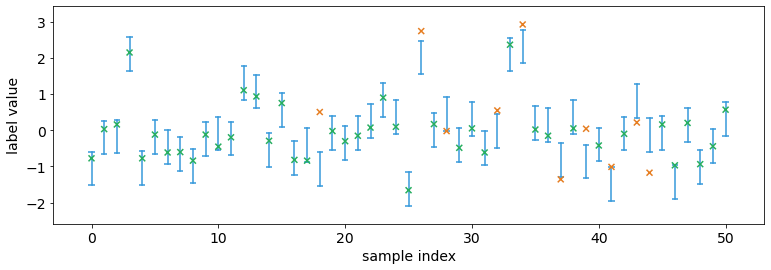

We used quantile predictions as an example. Note that we could use any prediction type as input. The following example uses point predictions

# Split the data into validation and test, in this example we will use quantile predictions as the original predictions

val_preds = reader['predictions_point'][:50]

test_preds = reader['predictions_point'][50:]

calibrator = ConformalIntervalPredictor(input_type='point', coverage='1/N') # The only difference from before is that the input_type is different

calibrator.train(val_preds, val_labels)

test_intervals = calibrator(test_preds, confidence=0.9)

interval.plot_interval_sequence(test_intervals, test_labels)

2. Online Conformal Prediction¶

In many applications, the data come in as a continuous stream. For example, we might make a prediction every day for tomorrow’s weather. After predicting tomorrow’s weather, we observe the true label before making a prediction for the-day-after-tomorrow’s weather. Torchuq supports this mode of prediction as well.

To make online predictions, the only new function you will need to know

is calibrator.update(predictions, labels). This functions works

almost identically as calibrator.train except it keeps the previous

validation data, while calibrator.train removes all validation data

and starts anew. The following example shows how to make online

predictions.

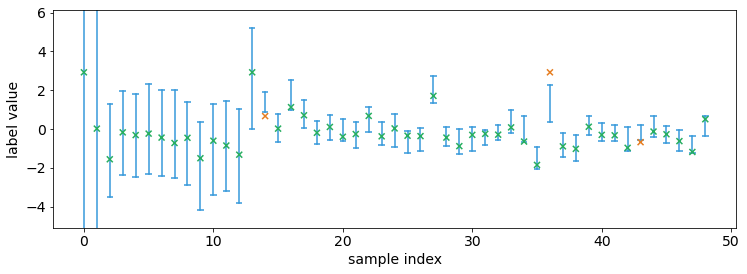

calibrator = ConformalIntervalPredictor(input_type='quantile', coverage='exact')

val_preds = reader['predictions_quantile'][:50]

val_labels = reader['labels'][:50] # Load the true label (i.e. the ground truth housing prices)

def simulate_online(calibrator):

# There needs to be at least 1 data point before making any prediction

calibrator.train(val_preds[0:1], val_labels[0:1])

prediction_history = []

for t in range(1, 50):

test_interval_t = calibrator(val_preds[t:t+1], confidence=0.9) # Make a prediction for the new time step

calibrator.update(val_preds[t:t+1], val_labels[t:t+1]) # Update the calibrator based on the observed label

prediction_history.append(test_interval_t)

# Concat the interval predictions for plotting

prediction_history = torch.cat(prediction_history)

return prediction_history

prediction_history = simulate_online(calibrator)

interval.plot_interval_sequence(prediction_history, val_labels[1:50])

Notably initially when there are very few observed data points, the

intervals are very large. This is because we selected

coverage='exact'. If we do not require exact coverage then the

interval sizes can be much smaller.

calibrator = ConformalIntervalPredictor(input_type='quantile', coverage='1/N')

prediction_history = simulate_online(calibrator)

interval.plot_interval_sequence(prediction_history, val_labels[1:50])

In fact, torchuq supports even more general prediction problems. For

example, we might make a prediction for the weather 7 days from today.

We will only observe the true label after 7 predictions. This is often

called online learning with delayed feedback. This can be achieved by

calling the calibrator.update function when the feedback arrives.